Check that you have a court order or formal agreement that qualifies for the relationship breakdown CGT rollover.

Relationship breakdown rollover

When 2 people separate or divorce, assets transferred between them usually qualify for the relationship breakdown rollover.

This means capital gains tax (CGT), which normally applies when ownership of an asset changes, is deferred. CGT will apply to the person who received the asset when they later dispose of it.

The relationship breakdown rollover of CGT only applies if assets are transferred under a court order or other formal agreement.

If the rollover applies to an asset, you must use it.

For a summary fact sheet with common scenarios about CGT and marriage or relationship breakdown and real estate transfers that you can download as a PDF, see Marriage or relationship breakdown and real estate transfers.

Qualifying agreements

The rollover applies to the transfer of assets (or other CGT events) that result from one of the following:

- a court order under the Family Law Act 1975, or a state, territory or foreign law relating to relationship breakdowns

- a court order made by consent under the Family Law Act 1975, or a similar foreign law

- an award made in an arbitration under the Family Law Act 1975 (section 13H), or a similar award under a state, territory or foreign law

- a financial agreement that

- is binding under the Family Law Act 1975 (sections 90G and 90UJ) or a corresponding foreign law

- meets the conditions for binding agreements

- a written agreement that is binding because of a state, territory or foreign law relating to relationship breakdowns, where the law prevents a court from making an order in relation to the agreement. The agreement must also meet the conditions for binding agreements. These agreements, known as 'binding agreements used by separating couples', are defined in each state and territory

- New South Wales: a domestic relationship agreement or termination agreement that complies with subsection 47(1) of the Property (Relationships) Act 1984 (NSW)

- Victoria: a relationship agreement that complies with subsections 59(1) and (2) of the Relationships Act 2008 (Vic)

- South Australia: a certified domestic partnership agreement within the meaning of the Domestic Partners Property Act 1996 (SA)

- Queensland: a recognised agreement within the meaning of the Property Law Act 1974 (Qld)

- Western Australia: a financial agreement that complies with subsection 205ZS(1) of the Family Court Act 1997 (WA)

- Tasmania: a personal relationship agreement or separation agreement that complies with subsection 62(1) of the Relationships Act 2003 (Tas)

- Australian Capital Territory: a domestic relationship agreement or termination agreement that complies with subsection 33(1) of the Domestic Relationships Act 1994 (ACT)

- Northern Territory: a cohabitation agreement or separation agreement that complies with subsection 45(2) of the De Facto Relationships Act (NT) .

From 1 July 2009, the marriage or relationship breakdown rollover is available to same-sex couples.

Conditions for binding agreements

For transfers that happen because of a binding financial agreement or a binding agreement used by a separating couple, the rollover only applies if, at the time of the transfer:

- the spouses are separated

- there is no reasonable likelihood of cohabitation resuming

- the transfer is for reasons directly connected with the breakdown of the marriage or relationship – this condition is not met if either

- the spouses had a pre-existing agreement that the asset was to be transferred between them for reasons other than the relationship breakdown

- the agreement provided for the transfer of non-specific property, which did not occur for a considerable time after the agreement (for example, more than 12 months) and was not clearly connected to the relationship breakdown.

Private or informal agreements

The rollover does not apply if you and your spouse divide assets under a private or informal agreement.

In this case:

- if you transfer an asset, you must report any capital gain or loss you make when completing your tax return for that year

- if an asset is transferred to you, it is treated as if you acquired it at the time of transfer.

The transaction is treated as if it was made at market value if both the following apply:

- the amount paid for the asset is greater or less than its market value

- the 2 former spouses are not dealing at arm's length.

CGT events the rollover applies to

The rollover applies to CGT events in which the transferor:

- transfers ownership of an asset to the transferee spouse (CGT event A1)

- enters into an agreement under which the right to use a CGT asset passes to the transferee spouse, and title in the asset passes to the transferee spouse at the end of the agreement (CGT event B1) (there is no rollover if title in the asset does not pass when the agreement ends)

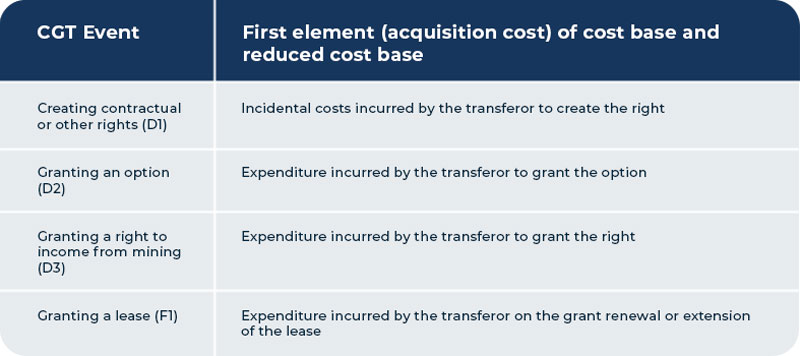

- creates a contractual or other right in favour of the transferee spouse (CGT event D1)

- grants an option to the transferee spouse, or renews or extends an option granted to them (CGT event D2)

- owns a prospecting or mining entitlement and grants the transferee spouse a right to receive income from operations carried on by the entitlement (CGT event D3)

- is a lessor and grants, renews or extends a lease to the transferee spouse (CGT event F1).

There is no rollover for the transfer of trading stock.

Timing of the CGT event

If an asset is transferred under a contract, the CGT event happens when the contract is entered into.

If there is no contract, the CGT event happens when the change of ownership of the asset occurs.

- A binding financial agreement may be a contract. A separation declaration must be made under section 90DA of the Family Law Act 1975 before the agreement can take effect.

- A binding agreement used by a separating couple may be a contract.

Transfers made because of a court order or arbitral award are not made under a contract. Therefore, the CGT event does not happen until the asset is transferred.

If CGT event B1 applies, the event happens when use of the asset passes to the transferee spouse.

How to calculate CGT on a rollover asset

If an asset is transferred to you under a relationship breakdown rollover, you do not pay capital gains tax (CGT) until you later dispose of it.

When you dispose of a rollover asset, you calculate your CGT as though you had owned it since your former spouse acquired it.

To calculate your capital gain or loss on the asset, take its capital proceeds (usually the amount you sold it for) and subtract:

- the asset's cost base at the time of the transfer – this is the first element of your cost base (the acquisition cost)

- any costs incurred in transferring the asset to you

- this may include conveyancing costs and stamp duty

- this does not include general legal costs relating to the relationship breakdown or property settlement

- any capital costs (that are not deductible against income) you incurred on the asset while you owned it.

If the asset was acquired by your spouse before 20 September 1985, it is not subject to CGT. Any subsequent major capital improvements to the asset are subject to CGT.

CGT discount on a rollover asset

To be eligible for the 50% CGT discount on an asset, you must have owned it for 12 months or more.

When working out how long you owned the asset, you include the period your former spouse owned it.

Superannuation assets

A CGT asset of a small super fund (one with no more than 6 members) can be transferred to another complying super fund under the relationship breakdown rollover. The consequences of the rollover are the same as for other transfers between spouses.

This allows spouses in a small super fund to separate their super arrangements on the breakdown of their relationship without any CGT liability.

Assets transferred by a company or trust

If a company or trust transfers a CGT asset to a spouse, the cost base and reduced cost base of interests in the company or trust need to be adjusted They are reduced in value by an amount that reflects the fall in their market value from the transfer of the CGT asset.

In some circumstances, the transfer of an asset from a company to a spouse who is a shareholder or an associate of a shareholder may be a dividend under Division 7A. In this case CGT does not apply.

If the transferor is a controlled foreign corporation or a foreign trust, there are special rules for working out the capital gain or loss for a subsequent CGT event.

Newly created assets

Your spouse (or a company or trustee) may create an asset in your favour.

For CGT purposes you acquire the asset at the time specified by the CGT event. For example, for CGT event D1, you acquire the asset at the time you enter into the contract or, if there is no contract, the time the right is created.

Relationship breakdown rollover and main residence exemption

When you sell a property that transferred to you under the relationship breakdown rollover, you may be eligible for the main residence exemption from capital gains tax (CGT).

You need to consider how you and your former spouse used the property during your combined period of ownership

Eligibility

Under the relationship breakdown rollover, there was no capital gain or loss for CGT purposes when your former spouse's share of the property transferred to you.

CGT was deferred, or 'rolled over', until you dispose of the property.

If the property was the main residence of you or your former spouse, you can generally claim a full or partial exemption from CGT when you dispose of it.

You are entitled to the full main residence exemption if the property is on land that is 2 hectares or less and:

- for property that transferred after 12 December 2006

- before the transfer, your spouse used the property as their main residence

- while you owned part or all of the property, you used it as your main residence

- the property was not used for rent or business

- for property that transferred on or before 12 December 2006

- after the transfer, it was your main residence and was not used for rent or business.

If you do not meet these conditions, you may still be entitled to a partial main residence exemption.

Calculating a partial exemption

Follow these steps to calculate the proportion of your share of the property that is subject to CGT.

Step 1: Work out the number of days after the transfer that the property was not your main residence.

Step 2: If the property was transferred to you

- after 12 December 2006, work out the number of days before the transfer that the property was not the main residence of your former spouse

- on or before 12 December 2006, the amount at this step is zero.

Step 3: Add the amounts from steps 1 and 2. This is the non-main residence days.

Step 4: Work out the total number of days that either you or your former spouse owned the share of the property. This is the total ownership days.

Step 5: Divide the amount at step 3 (non-main residence days) by the amount at step 4 (total ownership days).

The result is the proportion of the transferred share that is subject to CGT.

If you had joint ownership of the property before the relationship breakdown, the share you owned did not roll over. You simply continued to own it.

To calculate the proportion of your original share that is subject to CGT:

- work out the number of days during your ownership of part or all of the property that it was not your main residence

- divide this number by the total number of days that you owned part or all of the property.

Example: calculating CGT on a property transferred under the relationship breakdown rollover

George and Natalie jointly bought a holiday house.

- The sale settled on 14 March 2018.

- On 12 March 2020, George transferred his half share to Natalie under a relationship breakdown rollover.

- Natalie used the dwelling as her main residence for 3 years, from the date of the transfer until she sold it.

- Settlement of the sale was on 12 March 2023, at a price of $600,000.

- The cost base of the house was $400,000.

- Natalie's capital gain was $600,000 − $400,000 = $200,000.

Natalie is entitled to a partial main residence exemption because the property was used as a main residence for part of the combined ownership period.

Transferred share

The relationship breakdown rollover applies only to the half share transferred from George to Natalie.

The capital gain on this share is $200,000 × 50% = $100,000.

Using the steps above, Natalie calculates the assessable portion of her capital gain:

- Days after the transfer that the property was not Natalie's main residence:

0 - Days before the transfer that the property was not George's main residence:

730 - Add amounts from steps 1 and 2:

0 + 730 = 730 - Days in combined ownership period:

1,825 - Total non-main residence days ÷ total ownership days

730 ÷ 1,825 = 0.4

Natalie's assessable capital gain on the transferred share is:

$100,000 × 0.4 = $40,000

Natalie's original half share

The capital gain on Natalie's original half share is $200,000 × 50% = $100,000.

The property was Natalie’s main residence for 3 years out of the 5 years she owned her original half share. She works out the assessable portion of her capital gain as follows:

capital gain × (non-main residence days ÷ total ownership days) = assessable capital gain

$100,000 × (730 ÷ 1825) = $40,000

Capital gain to report

Natalie's total assessable capital gain for her original share and the transferred share is $40,000 + $40,000 = $80,000.

Natalie's ownership period is more than 12 months and she has no capital losses. Therefore, she can apply the 50% CGT discount to her assessable gain. The capital gain she reports in her tax return is:

$80,000 × 50% = $40,000.

Applying the ‘home first used to produce income’ rule

The home first used to produce income rule may apply if a property was:

- used as a main residence from the time it was acquired

- later used to produce income (such as renting it out).

Under this rule, the property is treated as if it was acquired for its market value at the time it was first used to produce income.

This rule applies to you if the property (or a share of it):

- transferred to you after 12 December 2006 under the relationship breakdown rollover

- was originally the main residence of you or your former spouse

- was first used to produce income (such as renting it out) after 20 August 1996. The first income-producing use may be during your or your spouse’s ownership period.

Example: main residence later used to produce income

Harry buys an apartment for $200,000 in 1999. He lives in it as his main residence.

A few years later, Harry and Anita marry. They move into Anita’s townhouse and Harry rents out his apartment. Its value is now $365,000.

In 2016, Harry and Anita's relationship breaks down. Harry transfers the apartment to Anita under a binding agreement and the CGT rollover applies.

Later, Anita sells the apartment. When working out the cost base, she uses the market value of the apartment when it was first used to produce income ($365,000), rather than its original purchase price ($200,000).

Nominating a main residence

In certain circumstances, spouses can choose how the main residence exemption applies to their property or properties.

For example:

- a spouse may be able to treat a dwelling as their main residence for a period even though they no longer live in it

- if there was a period before the separation when the spouses had different main residences, they must choose to either

- treat one of the properties as the main residence of both of them for the period

- nominate the different properties as their main residences and apply a part exemption to both.

Usually, such choices do not need to be made until lodging a tax return for the year in which a property is disposed of.

However, for the purpose of negotiating a property settlement, former spouses would generally nominate their choices before the transfer of property.

The transferor spouse could provide a signed statement to the transferee spouse at the time of the property settlement as evidence of making a choice.

The transferee spouse could use this statement to support their calculation of CGT in the future.

Once a choice is made, it cannot be changed.

Example: nominating a property as a main residence

Denise buys a townhouse and lives in it before starting a relationship with Calvin. She then moves into a rented apartment with him and rents out her townhouse.

Two years later, the couple buy a house and live in it together. Denise continues to rent out her townhouse.

Years later their relationship breaks down. Under a binding financial agreement, they agree that:

- Calvin will transfer his half share in the house to Denise, who will continue to live there

- Denise will transfer her townhouse to Calvin, who will live in it.

Because the townhouse had been Denise’s main residence, she can choose to continue treating it as her main residence for up to 6 years after she moved out.

In negotiating their binding financial agreement, Denise provides Calvin with a signed statement that she chooses to treat the townhouse as her main residence for the 2 years between when she moved out and when they bought the house together.

Because the home first used to produce income rule applies, Calvin treats the townhouse as if he acquired it for its market value at the time Denise first rented it out. The period prior to this, when the townhouse was Denise's main residence, is ignored. This period is not included in their combined period of ownership.

When Calvin later sells the townhouse:

- as a result of Denise’s choice, the townhouse is exempt from CGT for the 2 years from when she moved out of it until she and Calvin bought the house together

- the townhouse is exempt from CGT for the period he lived in it after the relationship broke down.

Foreign residents

You can claim the main residence exemption when you sell or dispose of a property as a foreign resident, provided:

- you have been a foreign resident for tax purposes for a continuous period of 6 years or less

- you experience a relationship breakdown or certain other life events.

Property transferred from a company or trust

You cannot claim the full main residence exemption on a property, or a share of a property, that transferred to you under a relationship breakdown rollover from a company or trust.

The main residence exemption only applies for the period you lived in the property after the transfer.

To calculate the proportion of your capital gain or loss that is exempt from CGT:

- work out the number of days the property was your main residence after the transfer

- divide this by the combined number of days it was owned by you or the company or trust.