Disposing of inherited assets

Generally, capital gains tax (CGT) does not apply when you inherit an asset.

When you sell an asset you have inherited, and the asset is:

- not a property, the normal rules apply for calculating your CGT

- a property, such as a house, it may qualify for the main residence exemption from CGT

- a collectable or personal-use asset, the normal rules apply – that is, the asset is subject to CGT unless it was acquired for less than the thresholds for these types of assets.

Cost of the asset

Unless the asset you inherit is fully exempt, you will need to know its cost base to work out your CGT when you sell it. Depending on the circumstances, the cost base may be based on the value of the asset:

- when the deceased acquired it

- when they died.

Eligibility for CGT discount or indexation

Australian resident individuals, trusts and super funds can use the CGT discount to reduce their capital gain on assets they have owned for 12 months or more.

For the purposes of qualifying for the CGT discount, you can treat an inherited asset as though you have owned it since:

- the deceased acquired the asset, if they acquired it on or after 20 September 1985

- the deceased died, if they acquired the asset before 20 September 1985.

If the deceased died before 21 September 1999, you have the option of indexing the cost base instead of using the discount. This involves calculating your capital gain by using the asset's cost base indexed for inflation up until 21 September 1999. If you use indexation, you are taken to have acquired the asset when the deceased acquired it.

Winding up a deceased estate

In administering and winding up a deceased estate, the legal personal representative (typically the executor) may need to:

- dispose of some or all of the estate's assets

- acquire an asset to satisfy a specific legacy and dispose of the asset to a beneficiary.

In these situations, CGT applies when the legal personal representative disposes of the asset. Any capital gain or loss made by the legal personal representative is subject to the normal CGT rules.

Unapplied capital losses

If the deceased had any unapplied net capital losses when they died, these do not transfer to you as a beneficiary or legal personal representative.

This means you cannot use any such losses to offset your net capital gains.

Keeping records of inherited assets

When you inherit an asset, it is important to keep records of:

- when the asset was acquired by the deceased

- the asset's value or cost

- costs related to the asset that are incurred by you and the legal personal representative of the deceased estate.

These records will help you work out your CGT when you later sell an asset.

If the deceased acquired an asset before 20 September 1985, you will need to know the asset's market value at the date they died.

- If the legal personal representative has had the asset valued, ask for a copy of the valuation report.

- If not, get your own valuation

If the deceased acquired an asset on or after 20 September 1985, you will need records of the deceased's cost base for the asset.

Assets passing to foreign residents

When an asset passes to a foreign resident, CGT applies to the deceased's estate at the time of their death if:

- the asset was acquired by the deceased on or after the start of CGT (20 September 1985)

- the deceased was an Australian resident when they died

- the asset is not taxable Australian property in the hands of the foreign resident beneficiary.

The capital gain or loss on the asset is worked out using:

- the market value of the asset at the date of death

- the cost base of the asset at that date (for a capital gain) or reduced cost base (for a capital loss).

The capital gain or loss must be reported in the deceased's date of death tax return.

Assets passing to charities and super funds

If a CGT asset passes to a tax-advantaged entity, CGT applies to the deceased's estate at the time of their death.

A tax-advantaged entity is either:

- a tax-exempt entity such as a church or charity

- the trustee of a

- complying super fund

- complying approved deposit fund

- pooled super trust.

The capital gain or loss on the asset is worked out using:

- the market value of the asset at the date of death

- the cost base of the asset at that date (for a capital gain) or reduced cost base (for a capital loss).

The capital gain or loss must be reported in the deceased's date of death tax return.

A capital gain or loss from a testamentary gift can be disregarded if both:

- the gift is made to a deductible gift recipient

- the gift would have been income tax deductible if it had not been a testamentary gift.

Cost base of inherited assets

How to work out the cost of an inherited asset when you calculate CGT.

Asset acquired by deceased before 20 September 1985

If the deceased acquired the asset before 20 September 1985, it was a pre-CGT asset while they owned it. The first element of your cost base – the acquisition cost – is the market value of the asset on the day the deceased died.

If the deceased made a major improvement to the asset on or after 20 September 1985, the improvement is not treated as a separate asset. You are taken to have acquired a single asset.

The cost base of this single asset is the total of:

- the cost base of the major improvement on the day the person died

- the market value of the pre-CGT asset, excluding the improvement, on the day the deceased died.

Asset acquired by deceased from 20 September 1985

If the deceased acquired the asset on or after 20 September 1985, the first element of your cost base – the acquisition cost – is generally the deceased’s cost base for the asset on the day they died.

However, the first element of your cost base is the market value of the asset on the day the deceased died if the asset:

- is a property that passed to you after 20 August 1996 (but not as a joint tenant), and just before the deceased died it was their main residence and was not being used to produce income

- passed to you as the trustee of a special disability trust.

Expenses the beneficiary includes in the cost base

As a beneficiary, you can include in your cost base (and reduced cost base) any expenditure a legal personal representative (LPR) would have included in their cost base if they had sold the asset instead of distributing it to you.

You include the expenditure on the date the LPR incurred it.

Example: transfer of an asset from executor to beneficiary

Maria died on 13 October 2022 leaving 2 assets:

- a parcel of 2,000 shares

- a vacant block of land.

The executor of the estate:

- disregarded any capital gain or loss on the transfer of the assets

- sold the shares to pay Maria's outstanding debts

- transferred the land to Maria's beneficiary, Antonio, and paid the conveyancing fee of $5,000 upon payment of all debts and tax.

The shares were not transferred to a beneficiary. Therefore, the executor must include any capital gain or loss on this disposal in the tax return for Maria's deceased estate.

The land was transferred to a beneficiary. Any capital gain or loss on this transfer is disregarded.

The first element of Antonio's cost base is Maria's cost base on the date of her death. Antonio can include the $5,000 the executor spent on the conveyancing in his cost base.

Legal costs incurred by a legal personal representative

As the LPR, in some circumstances, legal costs you incur may form part of the cost base of the estate's assets.

For example, if a LPR incurs costs to confirm the validity of the deceased's will or defend a claim for control of the estate, these costs form part of the cost base of the estate's assets.

Example: legal costs incurred to prove the validity of a will

Annie is the executor (LPR) of a deceased estate.

The deceased had more than one will prepared prior to their death:

- The final will left the estate’s assets to Max.

- Prior wills had left the estate’s assets to family members.

The family members challenged the validity of the deceased’s will in Court. As a result, Annie incurred legal costs on behalf of the deceased estate to defend this action.

The Court held that the final will was valid and granted probate.

The legal costs that Annie incurred to confirm the validity of the will and obtain probate were incurred to preserve or defend the rights over the estate’s assets.

Annie can't claim a deduction for these costs in her capacity as LPR as they are capital in nature. She can, however, include these legal costs in the cost base of the estate’s assets.

However, not all costs incurred by a LPR having a connection to estate assets will form part of the cost base of the estate's assets.

Example: legal costs incurred prior to the deceased’s death

Cassie is the executor (LPR) of a deceased estate.

Shortly prior to and in anticipation of the deceased’s death, Cassie acted as the solicitor for the deceased.

Cassie prepared an agreement for the transfer of interests in an asset to the deceased.

These actions were undertaken by Cassie prior to the deceased’s death and the commencing of Cassie’s duties as the LPR of the estate.

Any charges for Cassie’s solicitor services that are included in her charges as the LPR can't be included in the cost base of the estate’s assets.

However, such costs could form part of the cost base of the assets of the deceased at the date of death.

Indexing the cost base of an inherited asset

If the deceased died before 21 September 1999, you have the option of indexing the cost base when you dispose of the asset. Alternatively, you can claim the CGT discount. Usually, the discount will give you a better result.

With indexation, you calculate your capital gain by using the first element of the asset's cost base indexed for inflation up until 21 September 1999. You do not apply the discount.

If the deceased died on or after 21 September 1999, you cannot use indexation. If the deceased's cost base includes indexation, you must recalculate the first element of your cost base to exclude it.

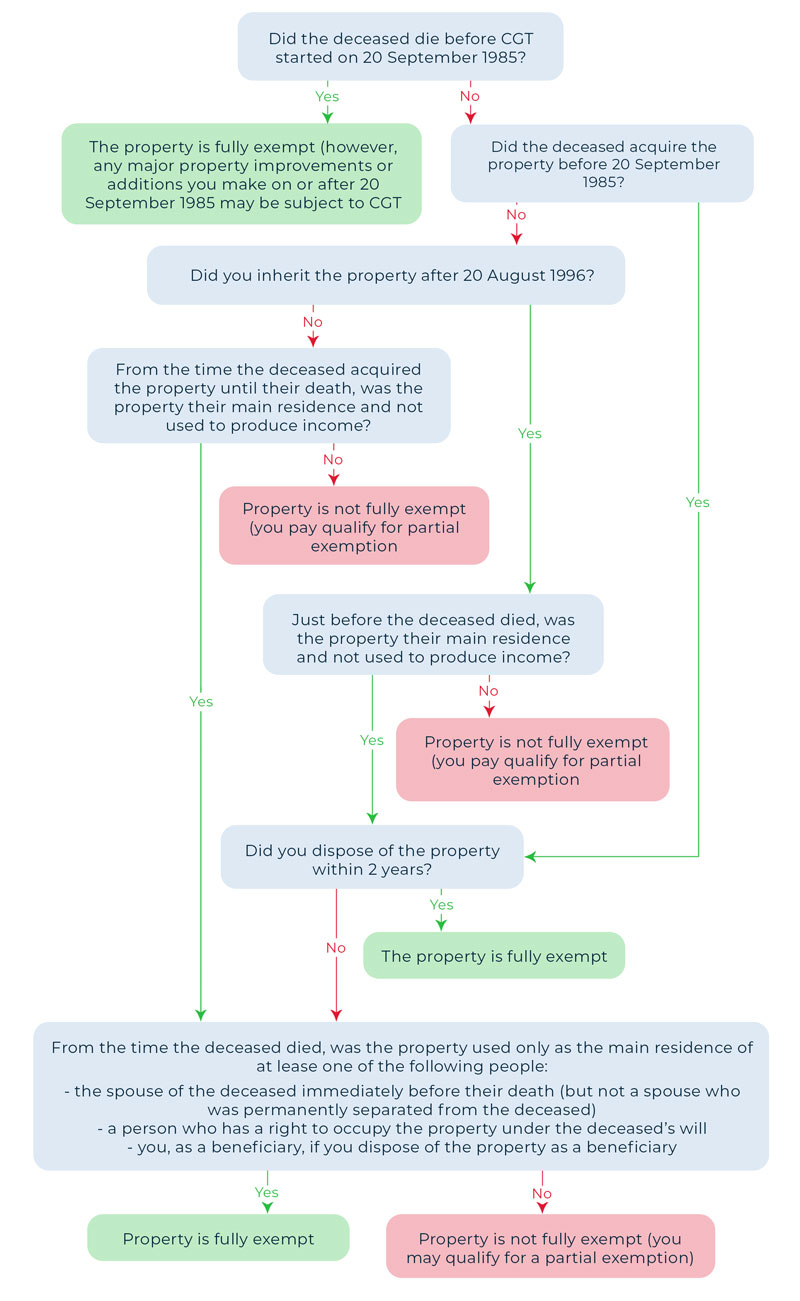

Inherited property and CGT

Find out if the inherited property is exempt from CGT, and what happens if there was more than one owner.

Work out if your inherited property is exempt

If you inherit a property and later sell or otherwise dispose of it, you may be exempt from capital gains tax (CGT).

The same exemption applies if you are the trustee of a deceased estate.

The inherited property must include a dwelling and you must sell them together. Generally, you cannot get a CGT exemption for land or a structure that you sell separately from the dwelling.

If you are a foreign resident, or the deceased was a foreign resident, you are generally not entitled to the main residence exemption when you sell the property.

Work through the following questions to find out if your inherited property is exempt from CGT.

Disposal within 2 years

You meet this requirement if you dispose of the property under a contract that settles within 2 years of the deceased's death.

It does not matter whether you used the property as your main residence or to produce income during the 2-year period.

You can extend the 2-year period if disposal of the property is delayed by exceptional circumstances outside your control.

Example: disposal within 2 years

Rodrigo was the sole occupant of a flat he bought in April 1990. He did not live in or own another property.

Rodrigo died in January 2023 and left the flat to his son, Petro.

Petro rented out the flat and then sold it 15 months after his father died.

Petro is entitled to a full exemption from CGT as he acquired the flat after 20 August 1996 and disposed of it within 2 years of his father's death.

Main residence while you own property

You meet this requirement if, from the deceased's death until you dispose of the property, both of the following are true:

- the property is not used to produce income

- the property is the main residence of at least one of the following people

- the person who was the spouse of the deceased immediately before the deceased's death (but not a spouse who was permanently separated from the deceased)

- a person who has a right to occupy the property under the deceased's will

- you, as a beneficiary, if you dispose of the property as a beneficiary.

The property can continue to be the main residence of one of the above people if they choose to treat it as their main residence (even if they have stopped living in it).

A property is considered to be your main residence from the time you acquire it if you move in as soon as practicable after that time.

Example: main residence while you own property

Peter bought a house prior to 20 September 1985. He died in February 1992 and the house passed to his beneficiary, Bob.

Under Peter’s will, Patti had a right to occupy the house. However, Patti could not move in until probate and administration of the estate was granted. During this period the house was vacant.

Probate and administration of the estate was granted in September 1992 and Patti moved in immediately.

Patti used the house as her main residence until Bob disposed of it in 2022.

Patti did not own any other property from the date of Peter’s death.

As Patti moved into the house when it was first practicable to do so, it is treated as Patti’s main residence from the time of Peter’s death until Bob sold it.

Bob is entitled to a full main residence exemption.

If your property is not fully exempt

If your property is not or only partially exempt from CGT, to work out your capital gain, you need to know its cost base.

If your property is partially exempt, you need to work out the proportion of your property that is exempt.

Foreign residents and inherited property

When you inherit Australian residential property:

- if the former owner of the property was a foreign resident for more than 6 years at the time of their death, you cannot claim the main residence exemption for the period they owned it

- if you have been a foreign resident for more than 6 years when you sell or dispose of the property, you cannot claim the main residence exemption for the period you owned it

- if you have been a foreign resident for 6 years or less when you sell or dispose of the property, to claim the main residence exemption you must satisfy the life events test.

If you are not entitled to the main residence exemption, CGT will apply when you sell or dispose of the property.

Example: inherit property from a foreign resident

Michael bought an Australian residential property in 2010 and lived in it as his main residence.

- On 1 July 2013, Michael moved to New York and rented out his Australian property.

- On 16 August 2021, Michael passed away.

- Anita, an Australian resident, inherited the property from Michael.

- Anita did not live in the property and sold it within 2 years.

At the time of his death, Michael had been a foreign resident for more than 6 years. This means Michael was not eligible for the main residence exemption at the time of his death, despite having lived in the property from 2010 to 2013.

Anita cannot claim the main residence exemption because Michael was not entitled to it. She must declare the capital gain in her tax return and pay CGT.

Right of survivorship

When the ownership of a property is shared and an owner dies, their share of the property is transferred based on their co-ownership arrangement.

How CGT applies to inherited assets

Disposing of inherited assets

Generally, capital gains tax (CGT) does not apply when you inherit an asset.

When you sell an asset you have inherited, and the asset is:

- not a property, the normal rules apply for calculating your CGT

- a property, such as a house, it may qualify for the main residence exemption from CGT

- a collectable or personal-use asset, the normal rules apply – that is, the asset is subject to CGT unless it was acquired for less than the thresholds for these types of assets.

Cost of the asset

Unless the asset you inherit is fully exempt, you will need to know its cost base to work out your CGT when you sell it. Depending on the circumstances, the cost base may be based on the value of the asset:

- when the deceased acquired it

- when they died.

Eligibility for CGT discount or indexation

Australian resident individuals, trusts and super funds can use the CGT discount to reduce their capital gain on assets they have owned for 12 months or more.

For the purposes of qualifying for the CGT discount, you can treat an inherited asset as though you have owned it since:

- the deceased acquired the asset, if they acquired it on or after 20 September 1985

- the deceased died, if they acquired the asset before 20 September 1985.

If the deceased died before 21 September 1999, you have the option of indexing the cost base instead of using the discount. This involves calculating your capital gain by using the asset's cost base indexed for inflation up until 21 September 1999. If you use indexation, you are taken to have acquired the asset when the deceased acquired it.

Winding up a deceased estate

In administering and winding up a deceased estate, the legal personal representative (typically the executor) may need to:

- dispose of some or all of the estate's assets

- acquire an asset to satisfy a specific legacy and dispose of the asset to a beneficiary.

In these situations, CGT applies when the legal personal representative disposes of the asset. Any capital gain or loss made by the legal personal representative is subject to the normal CGT rules.

Unapplied capital losses

If the deceased had any unapplied net capital losses when they died, these do not transfer to you as a beneficiary or legal personal representative.

This means you cannot use any such losses to offset your net capital gains.

Keeping records of inherited assets

When you inherit an asset, it is important to keep records of:

- when the asset was acquired by the deceased

- the asset's value or cost

- costs related to the asset that are incurred by you and the legal personal representative of the deceased estate.

These records will help you work out your CGT when you later sell an asset.

If the deceased acquired an asset before 20 September 1985, you will need to know the asset's market value at the date they died.

- If the legal personal representative has had the asset valued, ask for a copy of the valuation report.

- If not, get your own valuation

If the deceased acquired an asset on or after 20 September 1985, you will need records of the deceased's cost base for the asset.

Assets passing to foreign residents

When an asset passes to a foreign resident, CGT applies to the deceased's estate at the time of their death if:

- the asset was acquired by the deceased on or after the start of CGT (20 September 1985)

- the deceased was an Australian resident when they died

- the asset is not taxable Australian property in the hands of the foreign resident beneficiary.

The capital gain or loss on the asset is worked out using:

- the market value of the asset at the date of death

- the cost base of the asset at that date (for a capital gain) or reduced cost base (for a capital loss).

The capital gain or loss must be reported in the deceased's date of death tax return.

Assets passing to charities and super funds

If a CGT asset passes to a tax-advantaged entity, CGT applies to the deceased's estate at the time of their death.

A tax-advantaged entity is either:

- a tax-exempt entity such as a church or charity

- the trustee of a

- complying super fund

- complying approved deposit fund

- pooled super trust.

The capital gain or loss on the asset is worked out using:

- the market value of the asset at the date of death

- the cost base of the asset at that date (for a capital gain) or reduced cost base (for a capital loss).

The capital gain or loss must be reported in the deceased's date of death tax return.

A capital gain or loss from a testamentary gift can be disregarded if both:

- the gift is made to a deductible gift recipient

- the gift would have been income tax deductible if it had not been a testamentary gift.