Contributions and rollovers

As an SMSF trustee, you can accept contributions and rollovers for your members from various sources but there are some restrictions, mostly depending on the member’s age and the contribution caps.

You need to properly document contributions and rollovers, including the amount, type and breakdown of components, and allocate them to the members’ accounts within 28 days of the end of the month in which you received them.

From 1 October 2021 to rollover any super to or from your SMSF, you will need to use SuperStream.

Contributions you can accept

There are minimum standards for accepting contributions into your SMSF.

Allowable contribution

There are minimum standards for accepting contributions into your self-managed super fund (SMSF), and the trust deed of your fund may have more rules.

Whether a contribution is allowable depends on:

- whether you have the member's tax file number (TFN) – if not, you can't accept member contributions

- the type of contribution – for example, you can accept mandated employer contributions, such as super guarantee contributions from a member’s employer, at any time

- the age of the member – for example, you generally can't accept non-mandated contributions for members 75 years old or older

- whether the contribution exceeds the member's fund-capped contributions limit.

Generally, you can't accept an asset as a contribution from related parties of your fund, but there are some exceptions.

If your SMSF will receive contributions from employers (other than related-party employers), you'll need an electronic service address to receive the associated SuperStream data.

Member's tax file number

When a member joins your fund, you need to ask for their TFN and provide it to us. You can do this when you register the fund or when a new member joins.

A member is not required by law to provide their TFN, however if they don't:

- there may be administrative delays if the ATO can't identify the member from the other information you've provided

- your fund has to pay extra tax on some contributions made to that member’s account

- the member may not be able to receive super co-contributions

- your fund can't accept member contributions for them, such as personal and eligible spouse contributions.

If the member hasn’t provided their TFN and you’ve accepted member contributions for them, you’ll need to return the contribution within 30 days (of becoming aware of the contribution). However, if they provide their TFN within 30 days of receiving the contribution, you don’t have to return the amount.

If you receive employer contributions on behalf of a member and you pay additional income tax because you did not have your member’s TFN, you may be able to claim a tax offset in a later financial year if the member later gives you their TFN.

Mandated employer contributions

Mandated employer contributions are contributions made by an employer under a law or industrial agreement for the benefit of a fund member. They include super guarantee contributions.

You can accept mandated employer contributions for members at any time, regardless of their age or the number of hours they’re working.

Non-mandated contributions

Non-mandated contributions include:

- contributions made by employers over and above their super guarantee or award obligations (such as salary sacrifice contributions)

- member contributions – these are contributions made by or on behalf of a member, such as

- personal contributions

- eligible proceeds from primary residence disposal (downsizer contribution)

- super co-contributions

- eligible spouse contributions

- contributions made by a third party, such as an insurer

- re-contribution of COVID-19 early release superannuation amounts.

Non-mandated member contributions can only be accepted if you have their tax file number (TFN). If you receive a member contribution and you don’t have the member’s TFN, you need to return the contribution within 30 days unless the member’s gives you their TFN within that period.

You can accept non-mandated contributions in the following circumstances.

Members under 75 years old

From 1 July 2022, you can accept all types of non-mandated contributions, except downsizer contributions (these can only be made if the member has reached eligible age).

For a member turning 75, contributions must be received no later than 28 days after the end of the month they turn 75.

Between 1 July 2020 and 30 June 2022, you could accept all types of non-mandated contributions for members under 67. If they were between 67 and 75, you could only accept non-mandated contributions if they were gainfully employed on at least a part-time basis.

Before 1 July 2020, you could accept all types of non-mandated contributions for members under 65. If they were between 65 to 75, you could only accept non-mandated contributions if they were gainfully employed on at least a part-time basis.

Members 75 years old or over

You can accept downsizer contributions (there is no maximum age limit) if you have their TFN, but you generally can't accept other non-mandated contributions.

Super co-contributions and employer contributions that relate to a valid contribution period for the member can be accepted at any time.

Note: 'Gainfully employed on at least a part-time basis' means the member is gainfully employed for at least 40 hours in a period of 30 consecutive days in each financial year in which the contributions are made. Unpaid work does not meet the definition of 'gainfully employed'.

In specie (asset) contributions

'In specie' contributions are contributions to your fund in the form of a non-monetary asset.

Generally, you must not intentionally acquire assets (including in specie contributions) from related parties of your fund. However, there are some exceptions to this rule, including:

- listed shares and other securities

- business real property (land and buildings used wholly and exclusively in a business).

Contribution caps

Work out your concessional and non-concessional contribution caps by financial year.

Making contributions to SMSFs

A member whose total contributions exceed the contribution caps in a year may be liable for additional tax on the excess contributions. Contribution caps are indexed annually.

There are minimum standards for accepting contributions into your SMSF and the trust deed of your fund may have more rules.

Concessional contributions

Concessional contributions are contributions made into your SMSF that are included in the SMSF's assessable income. These contributions are taxed in your SMSF at a ‘concessional’ rate of 15%, which is often referred to as ‘contributions tax’.

The most common types of concessional contributions are employer contributions, such as super guarantee and salary sacrifice contributions. Concessional contributions also include personal contributions made by the member for which the member claims an income tax deduction.

Concessional contributions are subject to a yearly cap:

- From 1 July 2021, the general concessional contributions cap is $27,500 for all individuals regardless of age.

- For the 2017–18, 2018–19, 2019–20 and 2020–21 financial years, the general concessional contributions cap is $25,000 for all individuals regardless of age.

- For the 2014–15, 2015–16 and 2016–17 financial years, the concessional contributions cap is $30,000 per financial year and is increased to $35,000 for members 49 or over.

- For the 2013–14 financial year onwards, excess concessional contributions are no longer subject to excess contributions tax. If a member's contributions exceed the cap, the amount will be included in the member's assessable income and taxed at their marginal tax rate.

Unused concessional cap carry forward

From 1 July 2018, members can make 'carry-forward' concessional super contributions if they have a total superannuation balance of less than $500,000. Members can access their unused concessional contributions caps on a rolling basis for 5 years. Amounts carried forward that have not been used after 5 years will expire.

The first year in which you can access unused concessional contributions is the 2019–20 financial year.

Non-concessional contributions

Generally, non-concessional contributions are contributions made into your SMSF that are not included in the SMSF's assessable income.

Non-concessional contributions include:

- personal contributions made by the member for which no income tax deduction is claimed - this is the most common type of non-concessional contribution

- excess concessional contributions for the financial year which the member does not elect to remove from the superfund after the ATO send them an excess contributions determination will also count towards your member’s non-concessional contributions cap.

Non-concessional contributions do not include:

- super co-contributions

- structured settlements

- orders for personal injury or capital gains tax (CGT) related payments that the member has validly elected to exclude from their non-concessional contributions

- re-contribution of COVID-19 early release superannuation amounts made between 1 July 2021 and 30 June 2030. Individuals can re-contribute amounts they withdrew under the COVID-19 early release of super program without them counting towards their non-concessional contributions cap.

If a member’s non-concessional contributions exceed the cap, a tax of 47% is levied on the excess contributions. Individual members are personally liable for this tax and must have their super fund release an amount of money equal to the tax.

From 1 July 2022

From 1 July 2022, the non-concessional contributions cap is $110,000. Members under 75 years of age may be able to make non-concessional contributions of up to 3 times the annual non-concessional contributions cap in a single year.

If eligible, when you make contributions greater than the annual cap, you automatically gain access to future year caps. This is known as the ‘bring-forward’ option.

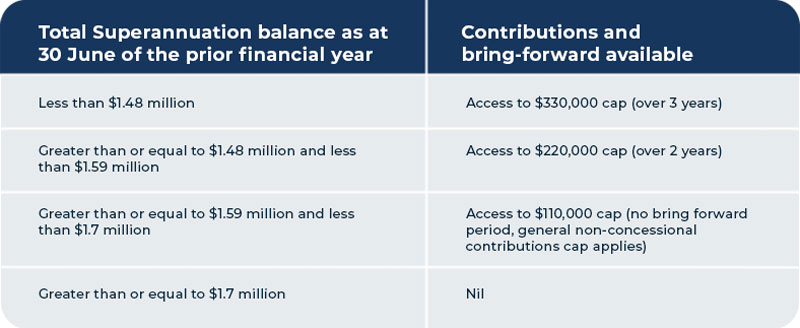

Bring-forward arrangements

From the 2022–23 financial year members who are under 75 may be able to access a bring-forward arrangement as outlined in the table below.

From 1 July 2021

From 1 July 2021, the non-concessional contributions cap increased from $100,000 to $110,000.

1 July 2017 to 30 June 2021

For the 2017–18, 2018–19, 2019–20 and 2020–21 financial years, the non-concessional contributions cap is $100,000.

1 July 2014 to 30 June 2017

For the 2014–15, 2015–16 and 2016–17 financial years, non-concessional contributions are subject to a yearly cap of $180,000 for members 65 or over but under 75 or $540,000 over a 3-year period for members under 65.

Transitional arrangements apply to individuals who brought forward their non-concessional contributions cap in the 2015–16 or 2016–17 financial years.

Rollovers

A rollover is when you, as a member, transfer some or all of your existing super between super funds, including SMSFs.

It is a legal requirement for rollovers to be processed electronically, using 2 components:

- a data message

- a separate payment transfer.

There are some exceptions.

Before making a rollover, there are several steps you need to complete to ensure it is successful.

Trustees must complete the rollover no later than 3 business days after receiving all the required information. Systems must be in place to action the requests. If your fund doesn't meet this requirement they could receive a compliance breach.

Personal contributions – deductions

If a member is eligible, they can claim an income tax deduction for super contributions they make for their own benefit. A member who intends to claim a deduction must notify you of this intent.

The member must give you the notice by the earlier of:

- the time they lodge their personal income tax return for the financial year during which the contribution was made

- the end of the financial year following the year the contribution was made.

The notice is invalid if:

- the person is no longer a member of your SMSF

- you no longer hold the contribution because of a partial rollover that included the contribution

- you have paid a lump sum or have started to pay a super income stream that includes the contribution.

In these circumstances, the member will not be able to claim a deduction for the personal contribution made.

Acknowledging valid notices

You must acknowledge your member's valid notice. Your acknowledgment should include:

- the date your fund received the notice

- any subsequent variations that your fund received

- member account and fund details

- the total amount of personal contributions that the notice covers

- the amount the member has notified you they intend to claim as a deduction

- the dates the contributions were made or the financial year they were made in.

This ensures that your members are able to claim the deductions they're entitled to and that super co-contributions and excess contributions tax are correctly applied.

You don't have to acknowledge the notice if the value of the relevant super interest on the day you received the notice is less than the tax that would be payable by you for the contribution.

Deadline for varying notices

If the member claiming the deduction has made an error with their notice of intent to claim a deduction, the notice can be varied (including varied to nil). Generally they need to do this by the same deadline as the original notice. After this, the notice can't be varied unless:

- a deduction for the contributions is not allowable (that is, the member was ineligible to claim a deduction)

- the variation reduces the amount shown on the original notice by the amount that is not allowable as a deduction.